Paul Reuge, European Equities Portfolio Manager Rothschild & Co Asset Management.

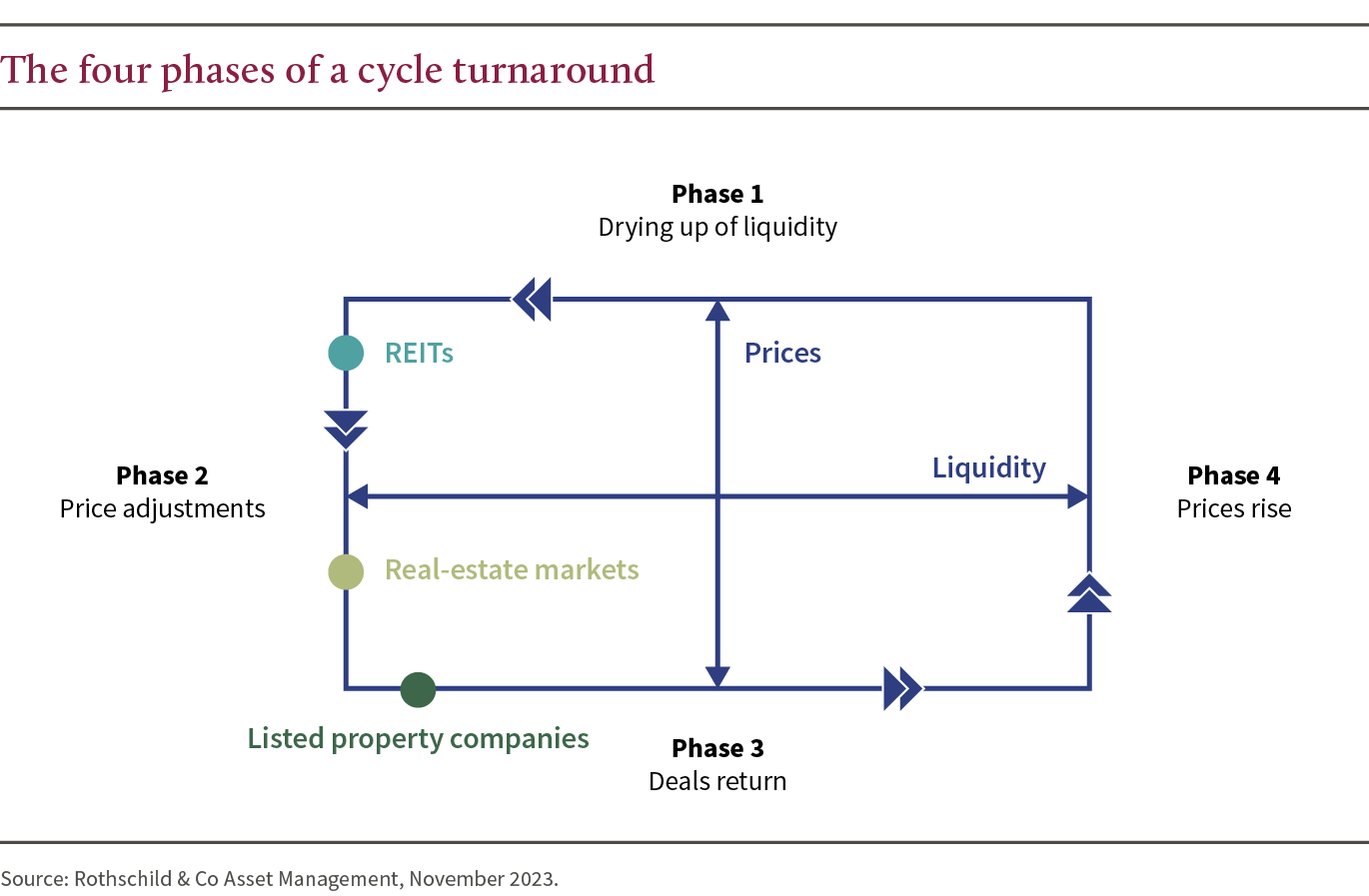

Each time the cycle turns, for whatever reason, what follows is a rather similar sequence that can be broken down into four phases.

The first is a drying up of liquidity as buyers and sellers fail to agree on a price due to a shift in the paradigm (in the present case, rising interest rates). Next comes the actual decline in prices (phase 2) until a new equilibrium point is reached that brings buyers back (phase 3), followed by the start of a new upward cycle (phase 4). The speed of adjustments depends on the type of vehicle used to invest in real estate. Naturally, the more liquidity there is, the faster the adjustment. That’s why listed property companies were the first to be sanctioned by the markets in 2022 via the sector’s significant correction (-37.57%(1)). Liquidity didn’t begin to dry up on the real estate markets until the second half of 2022. Real estate investment fund(2), meanwhile, saw their inflows adjust between six months and one year after the start of the crisis (in the first half of 2023).

An analysis of the two previous major real estate crises (in 1990 and 2008) shows that, on average, property companies begin their correction, and then rebound, one or two half-years before real estate markets do. In other words, if we assume that the real estate markets will bottom out in 2024, listed property companies should be close to a rally.

| Listed property cos. | Real estate markets | Real estate investment funds | ||||

| Peak | Trough | Peak | Trough | Peak | Trough | |

| Global Financial Crisis (2008) | Mars 2007 | Mar. 2009 | Q1 2008 | Q4 2009 | Aug. 2008 | Mar. 2009 |

| Lag | ~ +12 mths | ~ +8 mths | ~ +18 mths | – | ||

| 1990 crisis | Dec. 1990 | ~ 1995 | Q1 1991 | 1996 | Dec. 1992 | 1997 |

| Lag | + 3 mths | ~ +12 mths | ~+ 24 mths | ~ +24 mths | ||

| Current crisis | Dec. 2021 | [Mar. 23- Oct 23] | Q3 2022 | Estimated H1 2024 | Q2 2023 | ? |

| Lag | ~ +7/8 mths | ~ +7/8 mths | + 15 mths |

2024: the year that real estate bottoms out?

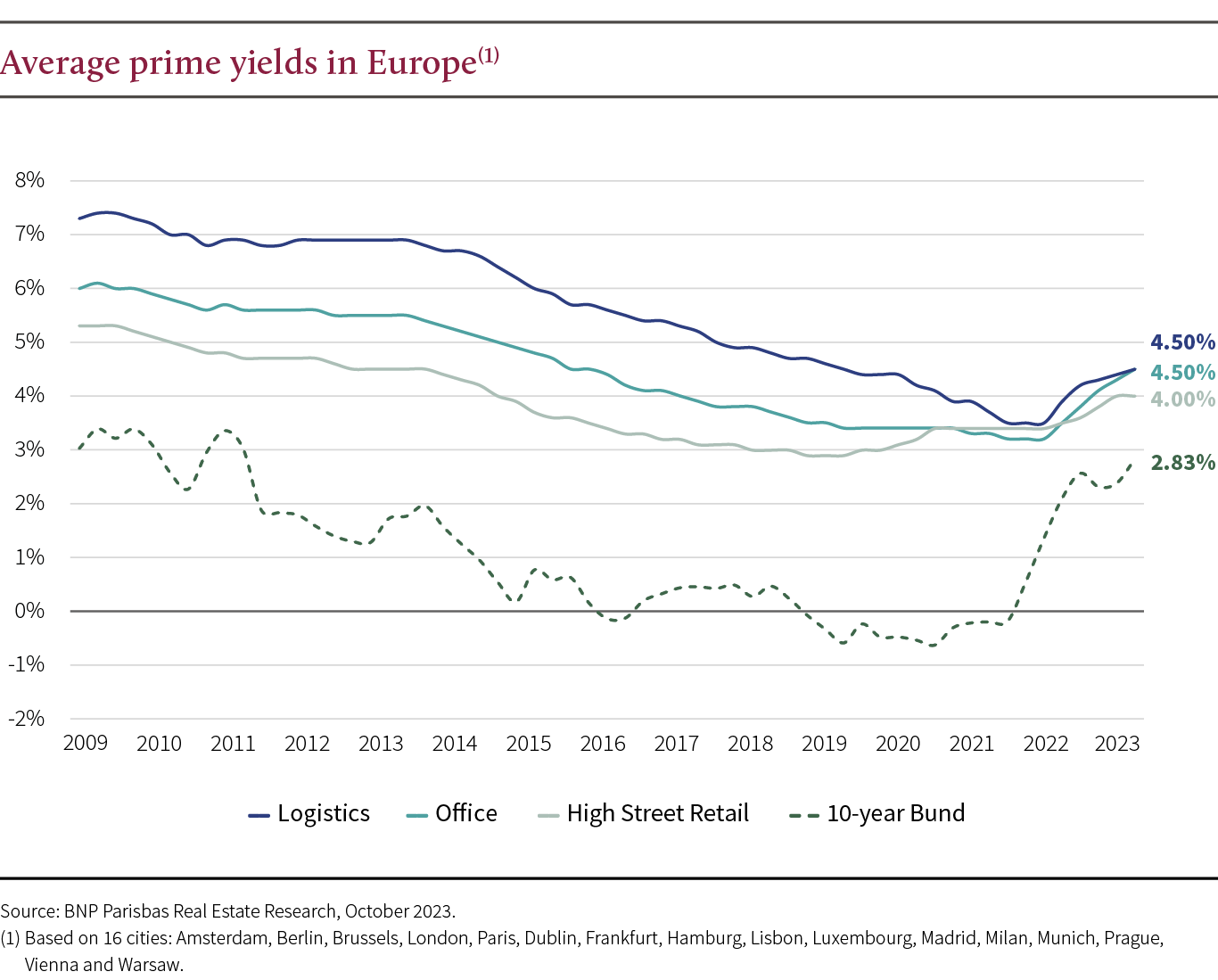

The average increase of yields by 100 to 150 basis points since the start of monetary tightening(3) was not enough to restore the complete risk premium of the previous decade. However, that was in an inflation-free world. The additional return that buyers can target, if rates do not decline (under a “higher-for longer” scenario) would therefore come from the inflation captured in rents:

So much of the adjustment to yields has already occurred, and the resiliency of rental markets (depending on the types of assets and location) has made it possible to limit the overall impact on the decline of market values. These have corrected since the market peak on average by -10% to -20%(4). Real estate brokers are thus expecting the decline to slow and to truly bottom out next year. The still significant discount on property companies (above 40%(4)) has provided additional room for depreciation, except in the case of logistics, where valuations are skewed by major development projects:

| Average value adjustment of prime asset between H1 2022 and H1 2023. | Estimated overall adjustment | Implicite value decline priced by the stock market since the peak | |

| Asset class | |||

| Offices | -15 % | [-20 % ; -25 %] | -30 % |

| Shopping centers(1) | -15 % | [-15 % ; -20 %] | -25 % |

| Logistics | -20 % | [-20 % ; -25 %] | -10 % |

| Healthcare | [-5 % ; -10 %] | [-10 % ; -15 %] | -20 % |

| German residential | -10 % | [-15 % ; -20 %] | -30 % |

(1) Average adjustment of premium asset values between H2 2019 and H1 2023

17 consecutive months of extreme discount: a new record!

Listed real estate has been trading at extreme discounts (of between 40% and 45%) since June 2022(4). This is the first time since the 1990s that we have experienced such a long phase of devaluation without a significant uptick. The constant postponement of the pivot (i.e., the end of monetary tightening) and the US regional banking crisis are why investors have waited so long to return to listed real estate. Property allocations in institutional portfolios are at a low(5).

Has the sector gotten through the worst of it?

In light of the above, there is reason to hope that this is so, barring a new crisis that might have (indirect) repercussions on property financing. In a less pessimistic scenario, the long maturity of companies’ liabilities (6 years on average), the available liquidity and the above-average quality of assets have enabled disposal programmes to continue in the current context (Unibail-Rodamco-Westfield has completed 90% of its €4 billion European disposal plan initiated in 2021, Covivio has sold €718 million since the start of the year, with a target of €1.5 billion by the end of 2024, Gecina €1.1 billion, etc.(6)) continue to provide strong security.

(1) Source: Institut de l’Epargne Immobilière et Foncière (IEIF) – Euro Zone (net dividend reinvested) – full-year performance 2022.

(2) unlisted.

(3) Source: Bloomberg, 31/10/2023.

(4) Sources: Companies (last reported net asset value) – Bloomberg 31/10/2023.

(5) Source: Exane, October 2023.

{kind=link}